The email arrives between two spam offers and an energy bill.

Subject line: “Changes to the taxation of your savings accounts.”

Most people tap it open in the supermarket queue or on the sofa, one eye on the TV and one thumb on their phone.

At first glance, the words look technical, almost dull. “New rate”, “withholding”, “from next month”. Then the key sentence jumps out: the government has confirmed a new tax will be taken directly from bank savings.

That quiet little pile of money that was supposed to be safe, growing slowly in the background.

Now it’s being shaved off before you even see it.

The day the rules changed for ordinary savers

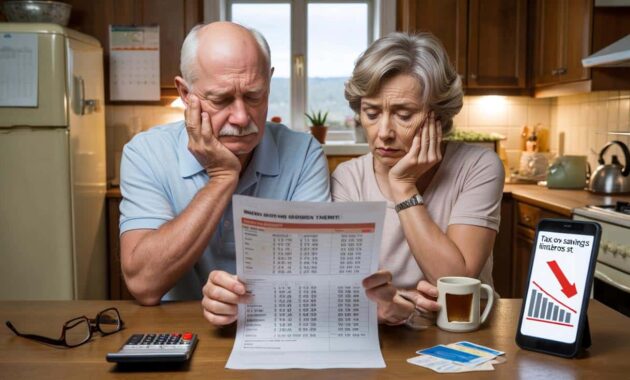

Picture a retired couple, Margaret and John, sitting at the kitchen table with two mugs of tea and a printed bank statement.

They’re not investors, not speculators, not playing the stock market.

Just two people who spent forty years putting small bits of money aside when they could.

On the page, the new line appears: “Tax on savings interest – debited”.

It’s not a fortune. £18.74 this month. But they look at each other in silence, and both are thinking the same thing.

If it’s £18 this month, what will it be in a year, in five years?

The rules of the game have changed.

And they didn’t get a vote on the small print.

What the government has confirmed is simple on paper: a new tax on the interest earned in bank accounts, to be applied automatically from next month.

No form to fill in, no box to tick. The money will be skimmed off before you ever touch it.

For millions of ordinary savers and pensioners, that means any interest above the existing allowance will now be partially redirected to the Treasury.

The stated goal is to “broaden the tax base” and “better align the treatment of capital and labour income.”

Big words that sound fair in a press conference.

But the reality is that it’s the savings of teachers, nurses, self‑employed workers and long‑retired factory staff that will quietly carry a new slice of the burden.

The people who play by the rules feel, once again, like the easiest target.

➡️ Microwaving a lemon : A simple kitchen trick you’ll keep using

➡️ Butter-free and barely sweet: the light, easy frangipane from a French dietitian

➡️ What the habit of piling clothes on a chair really says about you

On the government side, the argument is straightforward: public finances are stretched, debt is high, and the ageing population is putting pressure on pensions and health.

Tapping into savings interest looks like a neat technical fix.

It doesn’t show up as a “new big tax” on a payslip, and the amounts are fragmented across millions of accounts.

From a distance, it’s almost invisible.

From up close, it’s very visible if you’re relying on bank interest to top up a tiny pension or cover rising rent.

Let’s be honest: nobody really reads every line of the Finance Bill.

But this new rule doesn’t care whether people read it or not. It’s built into the system, silently clipping each pound of interest as soon as it appears.

That’s what makes so many savers feel less like citizens and more like a line in a spreadsheet.

How to react without panicking: concrete moves for your savings

Once the first shock passes, the question becomes practical: what can you actually do about this new tax?

The worst move is to do nothing for the next three years, then suddenly realise your savings have been eaten away more than you expected.

The first step is boring but powerful: list all your savings accounts and the interest rates they pay.

Not just your main bank, but that old account you opened ten years ago “just in case”.

Next, roughly estimate the interest you earn in a year and compare it to the tax‑free allowance that still exists for many savers.

If you’re over or close to the threshold, you have a decision to make.

Spread your money across different products, or look for accounts that remain sheltered from this new tax.

A single quiet evening with a calculator can be worth hundreds over the next few years.

A common instinct now is to pull all your money out of the bank and let it sit as cash “so they can’t touch it”.

It feels like a form of resistance, but it comes with other risks: theft, loss, and the slow erosion of value by inflation.

You dodge the tax but lose purchasing power month after month.

Another frequent mistake is to chase the highest interest rate without reading the conditions.

Some “promotional” accounts look generous, then lock your money for long periods or come with penalties if you need it back.

For anyone on a modest income, especially pensioners, flexibility often matters more than squeezing out an extra 0.3%.

We’ve all been there, that moment when you nod along to banking jargon just to avoid asking “Wait, what does that actually mean?”

This is one of those times where asking that question could literally pay off.

A financial adviser I spoke to put it bluntly: “This new tax won’t ruin the rich. It will nibble away at the cautious, the careful, the ones who quietly saved instead of spending everything.”

He pointed to three simple moves that ordinary savers can consider without diving into anything exotic or scary:

- Shift part of your savings into tax‑advantaged accounts that still exist under the new rules, even if the ceiling is lower than before.

- Diversify gently: a mix of instant‑access savings and low‑risk bonds can limit the tax hit while keeping your money accessible.

- Review your accounts once a year, ideally at the same time as you check your energy contract or insurance, so nothing drifts for a decade.

*None of this turns you into a day‑trader. It simply means you’re not leaving free money on the table in a system that already takes enough.*

A little awareness beats blind trust every single time.

Beyond the numbers: what this new tax really says about our social contract

Once you zoom out from the spreadsheets, this new tax reveals something deeper about how society treats small savers.

These are not people who benefited from huge property booms, complex tax schemes or corporate bonuses.

They are the backbone types: the ones who saved for Christmas, for a boiler breakdown, for the day work might suddenly stop.

For many of them, the interest on their savings isn’t a “bonus”.

It’s the difference between heating the house one degree higher in winter, or saying yes when a grandchild needs help with a deposit.

When that interest gets taxed, it’s those tiny, human decisions that get downgraded.

The plain-truth is that trust in institutions was already fragile.

Each quiet new charge, each unexplained line on a statement, chips away at it a little more.

Some will shrug and adapt. Others will feel that the deal they thought they had with the state – work, save, be responsible, and you’ll be respected – has been quietly rewritten without their consent.

| Key point | Detail | Value for the reader |

|---|---|---|

| Know what’s taxed | Only interest above the existing allowance is affected, and the tax is taken at source by the bank. | Helps you estimate the real impact on your monthly and yearly income. |

| Map your savings | List all accounts, rates and annual interest, including old or forgotten accounts. | Gives you a clear picture so you can shift money where it’s treated more fairly. |

| Adjust calmly | Use tax‑advantaged products, diversify gently, and review your setup once a year. | Reduces the long‑term bite of the tax without taking reckless risks. |

FAQ:

- Question 1Will the new tax hit every single saver, no matter how small their account?

- Question 2How will I see the new tax on my bank statements each month?

- Question 3Are pensioners or low‑income households getting any specific protection?

- Question 4Should I move my savings into investments like shares to avoid this tax?

- Question 5Can the government increase this tax again in the future if public finances worsen?